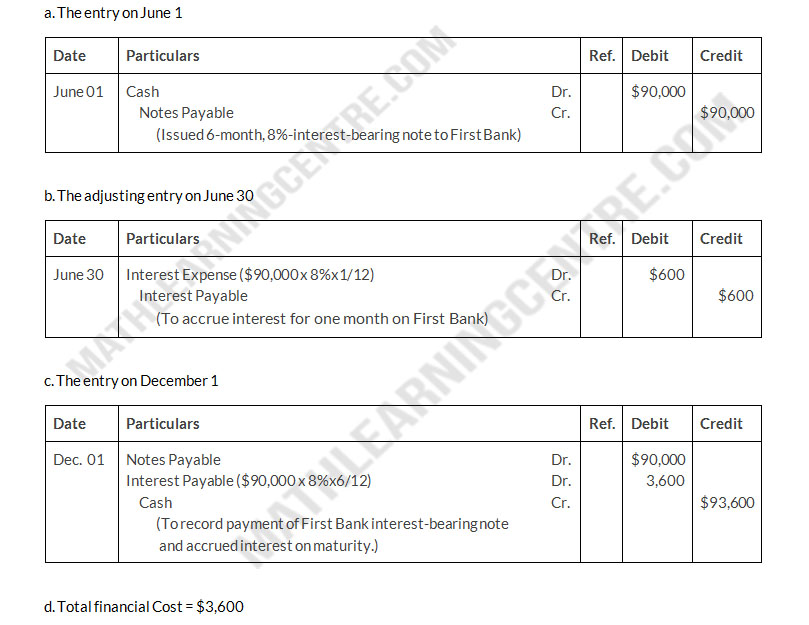

Istisna ic agreements eg Ijarah (lease) and you can Musharakah Mutanaqisah (Shrinking Relationship). The combined access to this type of deals lets banking institutions and you can developers in order to mobilise money and you may decrease risks. Such as, the newest expansion away from Madinah Airport into the Saudi Arabia utilised Istisna and you may Ijarah as long label financial support preparations (Industry Lender, 2017). Earliest, the project team import certain legal rights so you’re able to financiers (lenders) below good procurement agreement (Istisna) plus the payment is disbursed considering a conformed plan. Lenders likewise have concession arrangements (Ijarah) for the venture business and receive lease accommodations due to the fact money. For example an arrangement is frequently used in capital intensive structure strategies (Chu and Muneeza, 2019).

Not as much as a mix of Istisna and Musharakah Mutanaqisah, the customer and bank perform a Musharakah pool underneath the principle from shirkahtul-whole milk and as one enter a keen Istisna package for the company/creator towards given resource design (Lender Negara Malaysia, 2015a). Into the funding several months, possession try gradually gone to live in the consumer up until full fee is generated.

step 3.step three.step 1. Exposure doing work in Istisna

Islamic financial institutions that offer Istisna are exposed to liquidity, operational and ). Similarly to Ijarah Muntahiya Piece Tamlik, market value fluctuation may result in an alternative value of within this new beginning date. The fresh loan providers are liable for low-birth if there is incapacity doing the building venture on time, pricing overruns and force majeure occurrences (IFSB, 2015). Such as for instance working exposure leads to exchangeability chance as the earnings of your organization may be affected in the event the investment isnt accomplished at offering big date. These threats aren’t typical to have traditional finance companies given that completion chance is generally borne because of the enterprise team.

Although the Istisna’ bargain is permissible of the Islamic scholars, multiple Shariah circumstances comes up along the implementation of Parallel Istisna deals. The initial issue is cost: Istisna try an onward revenue bargain where in fact the item is actually not brought yet , which means that choosing the expense of the commodity was subject to conjecture, which is blocked significantly less than Shariah rules.

To get over this problem and steer clear of gharar, Bank Negara Malaysia (2015b) released the guidelines to your Istisna, and this reported that the price of new Istisna resource have to be based on shared agreement by hiring functions (agreed price) at the time of entering into the fresh bargain. Furthermore, brand new arranged cost of the newest advantage may be modified immediately following entering on the price and before birth of your Istisna investment to help you the buyer.

cuatro. Discussion

In this section, items according to Islamic home financing would be talked about. It looks during the intricacies out-of resource assets less than build, the fresh new more than likely dangers inside it, rebates, charges and rehearse of interest cost for benchmarking.

To order a property below structure is far more complicated than just to buy a beneficial freshly mainly based family around Islamic law. Istisna are an enthusiastic Islamic price getting homebuyers to purchase property lower than construction; but not, that it contractual arrangement ic economic intuition. Financial Negara Malaysia (2015a) stated that for the true purpose of obtaining a secured asset less than framework, loan providers could possibly get arrange Musharakah Mutanaqisah that have Istisna for which brand new people go into a keen Istisna bargain with an authorized. The Istisna principle allows the new offering out-of something which isnt developed or is under build. For this reason, rather than most other contracts, a keen Istisna deal are far more suitable given that a home financing tool in the event that house is not offered but really or not a great ready-stock domestic.

The fresh new Musharakah Mutanaqisah offer is much more versatile as compared to Murabahah and you may Ijarah Muntahiya Piece Tamlik deal when it comes to rates. When you look at the Musharakah Mutanaqisah, the bank is also adjust the newest leasing price with regards to the newest market value which means that each other visitors and speedycashloan.net payday loan no fax you can lender are not opened to offer chance. The customer tends to make occasional instalments according to an industry valuation, and price is dependent on the marketplace value at the period, which includes a lesser amount of sector exposure versus Murabahah/BBA funding. The price of the house or property try pre-determined in a keen Istisna price. The foundation of the Shariah specifications is that the speed become recognized will be to clean out suspicion one ). Deferred fee are greeting from inside the an Istisna bargain.