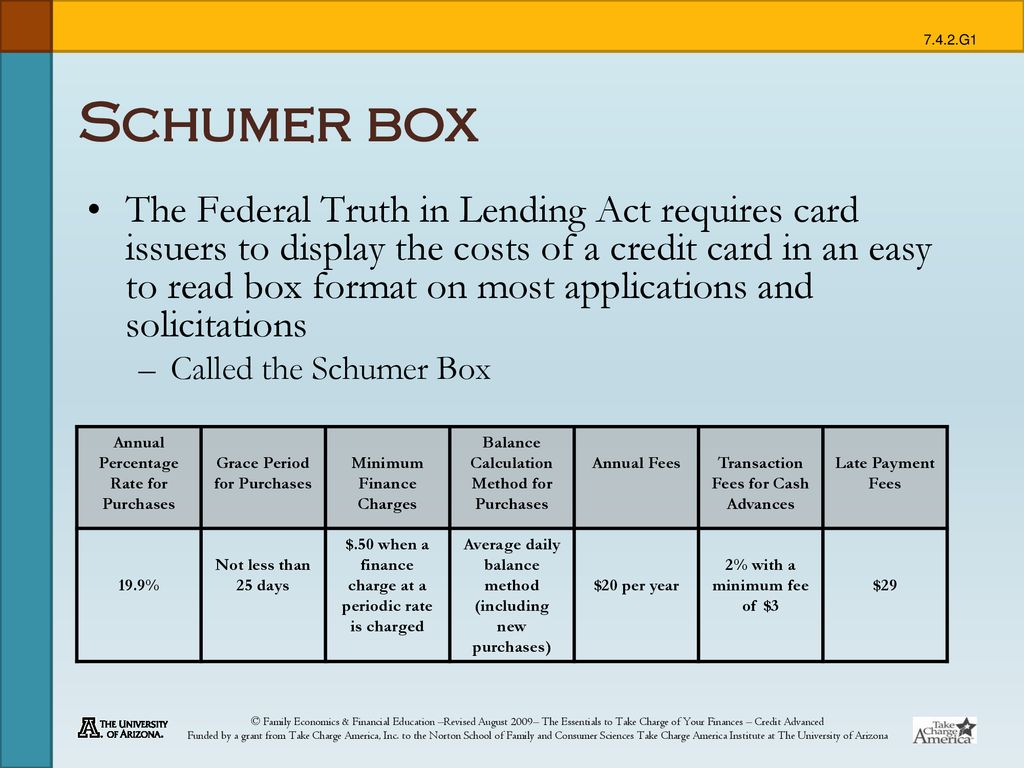

Verification regarding Manager-Occupancy For everybody financing protected from the a main household which might be selected via the random selection techniques (and for fund chosen from the discretionary options process, because the appropriate) the latest blog post-closure QC review need to is verification away from owner-occupancy. The lending company have to feedback the house insurance or other records from the file (particularly, assessment, income tax output otherwise transcripts) to verify that we now have no symptoms that house is not the borrower’s dominating quarters.

Separating it from the six months output a monthly shot sized forty financing

That doesn’t mean every financing is totally audited getting proprietor occupancy, but a particular fee is actually, and people that have red flags are certainly examined. Be mindful available to choose from!

The agency funds possess some quantity of QC comment and you will audit

Used to do it, also refinanced later. The major thing is your intent, for many who go into the home loan understanding you aren’t browsing real time indeed there, however, simply leaves they blank, then you need declare it as a secondary residence. It doesn’t mean you could book they even in the event in many (most?) home loan deals, usually you cannot do it once about a-year unless of course your claim up front your own intention in order to rent or take a great highest rate of interest.

During my circumstances I bought, but decided not to provide me personally to sell another family, thus i only use the fresh new set just like the an intermittent freeze mat and financing (this has enjoyed much). We stated it a vacation whenever i refinanced, the initial home loan it was stated because the primary to your financial once the that was my intention at the time.

My personal information are getting 100% sincere with someone (mortgage company/underwriter, insurance coverage, HOA etcetera), for those who rest, you merely provide them with every a justification/beginning to help you gap your own home loan otherwise even worse – insurance, should you ever want to make a state. You truly just damage yourself by the sleeping otherwise misleading.

ChicagoBear7 blogged: ^ Fri Dislike https://paydayloansconnecticut.com/shelton/ to burst everybody’s bubble, but there’s a complete world out of mortgage quality-control audit companies available to choose from. Associated with contained in the Freddie and Fannie guidance. We have found off Fannie’s:

Verification regarding Holder-Occupancy For everyone money secured by the a principal quarters that will be chose via the haphazard alternatives process (and money picked from discretionary choice techniques, as relevant) the brand new blog post-closing QC review need to are verification off manager-occupancy. The lending company need to comment the property insurance plan or other documentation regarding the document (for example, appraisal, tax productivity or transcripts) to verify there exists no symptoms your property is perhaps not new borrower’s principal home.

Separating so it because of the 6 months productivity a month-to-month shot measurements of 40 finance

That does not mean the mortgage is totally audited to own owner occupancy, however, a certain fee try, and the ones that have red flags are definitely analyzed. Be careful nowadays!

”Therefore, a loan provider originating typically 1,000 financing 30 days might guess good 6-month society of 6,000 funds. And if an expected incidence rate (otherwise problem rate) of 5% and you can a precision target out-of 2%, the fresh new resulting Sample Proportions will get 242. ”

What is actually unclear is exactly what happens when failing is understood – ’s the failure remediated, or perhaps is the QC incapacity merely regularly create a reasoning of looks out-of mortgages overall?

You can purchase your loan that have step three.5% or more down and possibly a sandwich 3% interest rate. Individuals taking a loan purely for the intended purpose of that have good leasing assets must constantly set-out 35%, show questioned rents compared to rates, and certainly will have in all probability to pay cuatro% or maybe more pricing.